She is being sold Down from 1.40 to close at 1.30, I see great opportunity is back!

The profit guidance is being impact by once-off amount of about 83m. It will still be profitable for 1st half as well as FY 2023! I think interim dividend of 4 cents and final dividend of 4.5 cents would not be affected.

Yield is a whopping 6.53% at 1.30.

When the mkt is fearful, I am seeing golden opportunity!

Please dyodd.

She will be reporting her 1st Half 2023 results on 11th August cum interim dividend of 4 cents.

One of the rare commodity counter listed locally.

If the listing of IPO get the approval from Saudi side then price may get lifted again. And the 2nd IPO to be listed on London if also able to carry out later on then we may see further catalyst to drive the price further.

Not a call to buy or sell!

Please dyodd.

We’re a leading food and agri-business, supplying food ingredients, feed and fibre to thousands of customers worldwide, from world famous brands to small family run businesses.

Our global team of employees has built leadership positions in businesses such as cocoa, coffee, cotton, nuts and spices.

Headquartered and listed in Singapore, we rank

among the top 30 largest primary listed companies in Singapore in terms of market capitalisation on SGX-ST. We are a Fortune Global 500 company and since June 2020 we have been included in the FTSE4Good Index Series.

In January 2020, we announced a Re-organisation Plan to create distinct and coherent operating groups – ofi, Olam Agri, and the Remaining Businesses of Olam Group – to maximise long-term value on a sustained basis.

Each operating group has developed a clear Purpose, compelling vision and a differentiated strategy to capitalise on specific trends that underpin its sectors, take advantage of market opportunities, attract talent, optimise resources and invest in requisite assets and capabilities which will deliver profitable growth and build long-term value on a sustained basis.

ofi: Naturally good food and beverage ingredients and solutions

Olam Agri: Transforming food, feed and fibre

Remaining Businesses of Olam

We are exploring strategic options to maximise the value of the Remaining Businesses of Olam comprising Nupo Ventures - our incubator and start-up businesses, Mindsprint - providing shared services to the operating groups, and Olam Global Holdco - which holds the de-prioritised and gestating assets.

A Taste of What We Do

Our value chain spans over 60 countries, from growing crops in our own orchards and estates, to sourcing from a global network of farmers. We operate over 80 large processing and manufacturing facilities, developing and delivering food ingredients, feed, and fibre, alongside supply chain, trading and risk management expertise to support our customers’ needs. Additionally, We market our own brands directly to consumers in Africa.

The listing of ipo for Saudi side still hasn't gotten the approval yet! Sgx side already approved. This is taking longer than expected!

So, 1st half of 2023 is not possible!

Need to wait for further announcements!

Share price kena sold down from 1.47 to 1.36, seem overly done.

It has bounced off from 1.36 to close at 1.42 seems rather interesting!

Yearly dividend of 8.5 Cents.

Yield is a whopping 6.07% at 1.40.

Pls dyodd.

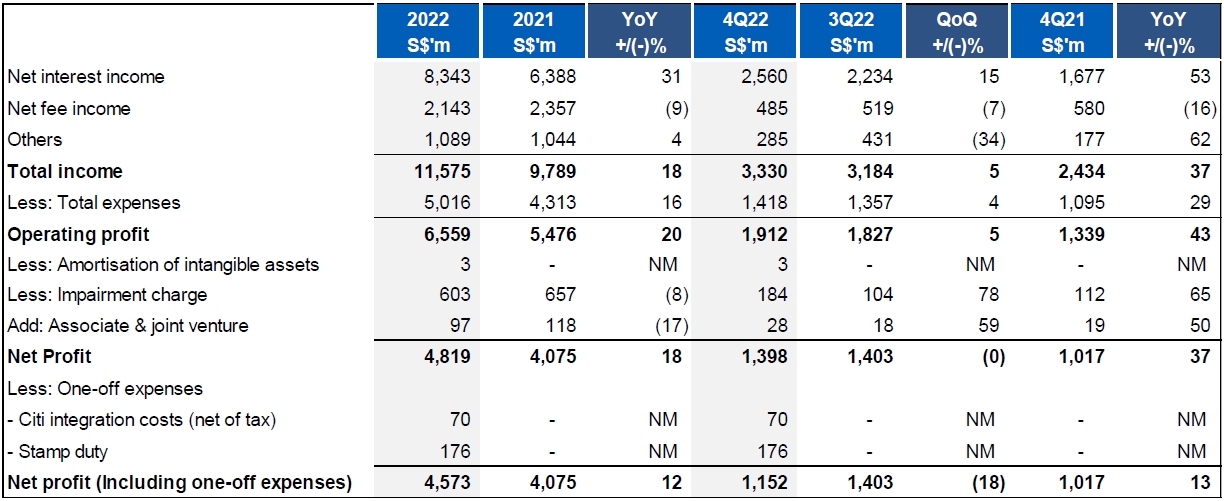

Olam FY2022 results are as follows:

Nibbled a bit at 1.40 for quite a gd dividend yield of more than 6% yield.

Forst Half 2023 Results will be out on 11th August 2023.

NAV 1.838.

Pls dyodd.